Lenskart, India’s leading eyewear retailer, is preparing for an IPO slated for November 2025 with a market valuation near ₹70,000 crore ($8 billion). This valuation is considered very high given the company’s financial metrics and market position, leading many analysts and investors to view Lenskart as overpriced.

Market Valuation and Financials

At its IPO price band of ₹382 to ₹402 per share, Lenskart aims to raise around ₹7,278 crore through a combination of fresh equity and an offer-for-sale by existing shareholders. The company reported net profits of approximately ₹297 crore in FY25 on revenues of about ₹6,650 crore. This was the first year Lenskart reported profitability after years of operational losses.

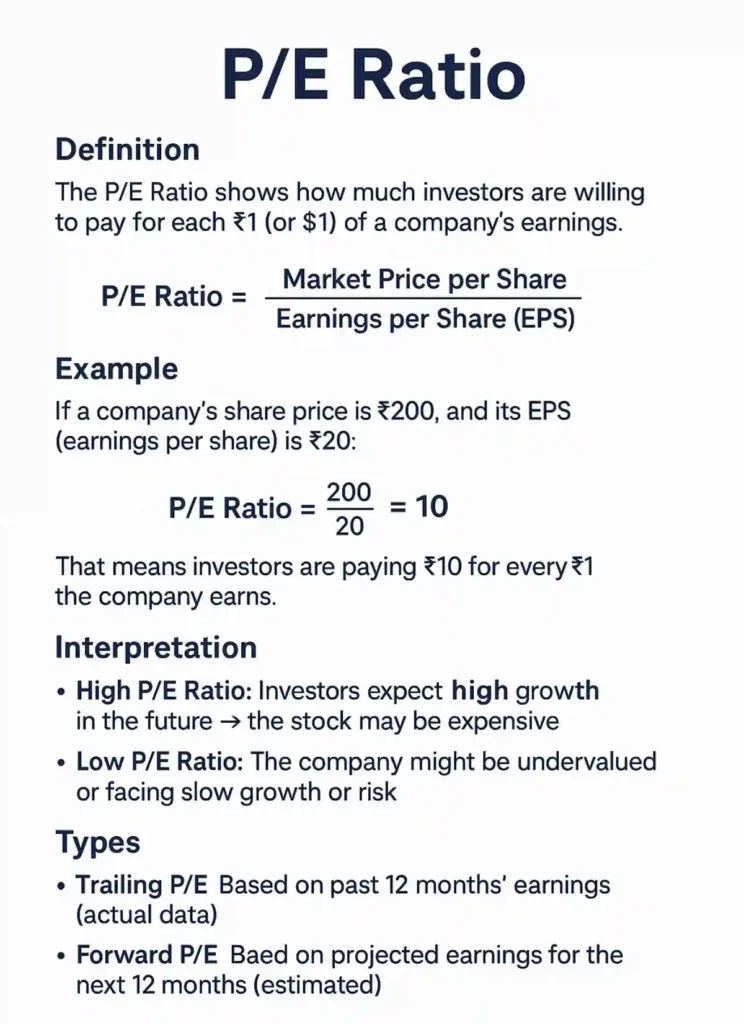

Despite turning profitable, Lenskart’s price-to-earnings (P/E) ratio stands around 237, which is exceptionally high for a consumer retail company. The price-to-sales ratio is close to 10.5x, and the price-to-EBITDA multiple is approximately 70x, both significantly above industry averages. Much of the reported profit was aided by non-recurring accounting gains related to the revaluation of deferred payments from its acquisition of the Japanese eyewear company Owndays, inflating profitability figures [removal of references applied].

Reasons for Overpricing

- Extremely High Valuation Multiples: Lenskart’s P/E ratio of 237 times earnings far exceeds that of other retail and consumer tech companies, suggesting expectations of very rapid growth and margin expansion. This level of optimism prices in substantial future performance risks.

- Accounting Gains Inflating Profitability: The profitability in FY25 is not entirely from core operations but partly from one-time accounting adjustments, making the earnings figure less reflective of sustainable business performance.

- Promoter Share Sale Signals: Co-founder Peyush Bansal had purchased shares at a much lower valuation months ago but is now selling shares at nearly nine times that price, which raises concerns about the true intrinsic value of the company.

- Comparisons With Peers: Compared to established players like Titan Eye+ or other consumer retail brands, Lenskart’s multiples are notably higher despite having a shorter profit track record and being a newer entrant in physical retail.

- Heavy Reliance on Projected Growth: The company’s valuation assumes aggressive growth—anticipating a 33% compound annual growth rate in revenues and rapid expansion of store footprints. Any failure to meet these ambitious targets could affect market sentiment and stock pricing.

In summary, while Lenskart is the dominant player in India’s eyewear market with strong growth prospects, the IPO valuation is steep and not fully supported by its current financials. Its high P/E ratio, reliance on accounting profits, and aggressive growth assumptions make the stock appear overpriced, warranting caution from investors considering entry at this level.