Gurugram-based pesticide manufacturer Mahamaya Lifesciences Limited is set to make its stock market debut with an Initial Public Offering (IPO) that opens for subscription on November 11, 2025. This SME IPO on the BSE platform has generated significant interest among investors seeking exposure to India’s rapidly expanding agrochemical sector. With a remarkable 148% profit surge in FY 2025 and strategic expansion plans, the company presents an intriguing investment opportunity. However, the current Grey Market Premium (GMP) of ₹0 suggests cautious investor sentiment. Let’s dive deep into whether this IPO deserves your hard-earned money.

- Company Business Overview

- IPO Issue Details

- Key IPO Dates

- Issue Registrar and Lead Manager

- Objects of the Issue

- Company Financials (₹ in Crores)

- Grey Market Premium (GMP) Analysis

- Peer Comparison Analysis

- Broker Recommendations

- Strengths and Competitive Advantages

- Challenges and Risk Mitigation

- Growth Drivers and Future Outlook

- Valuation Assessment

- Application Strategy

Company Business Overview

Mahamaya Lifesciences Limited, incorporated in 2002, specializes in the manufacturing of pesticide formulations and supplying bulk technical products to both Indian agrochemical companies and multinational corporations (MNCs). The company has carved a niche in importing and registering vital pesticide molecules that were not domestically produced in India.

The company’s business model involves working closely with the Central Insecticides Board and Registration Committee (CIBRC) under the Department of Agriculture, Government of India, to register imported pesticide molecules. After successful registration, these molecules are marketed both as technical products and value-added end-use formulations.

Key Products Portfolio

Mahamaya Lifesciences manufactures several critical pesticide formulations including:

- Emamectin Benzoate (Technical and Formulations) – flagship product

- Glufosinate Ammonium – introduced in recent years

- Tolfenpyrad – new-generation insecticide

- Abamectin – broad-spectrum insecticide

- Acetamiprid – neonicotinoid insecticide

- Atrazine – herbicide

- Imidacloprid – systemic insecticide

- Bispyribac Sodium – selective herbicide

Manufacturing Facilities

The company established its own manufacturing plant in December 2021 at Dahej, Gujarat, marking a significant milestone in its growth journey. This facility enables the company to maintain quality control and reduce dependence on external manufacturers.

Market Presence

Domestic Market: The company’s products reach various states including Punjab, Haryana, Rajasthan, Uttar Pradesh, Gujarat, Maharashtra, Andhra Pradesh, and Telangana.

Export Markets: Mahamaya exports to Turkey, Egypt, UAE, Qatar, Dominican Republic, and has recently expanded into USA and Hong Kong. Export sales contribution increased from 2.17% in FY 2024 to 4.70% in FY 2025, demonstrating growing international acceptance.

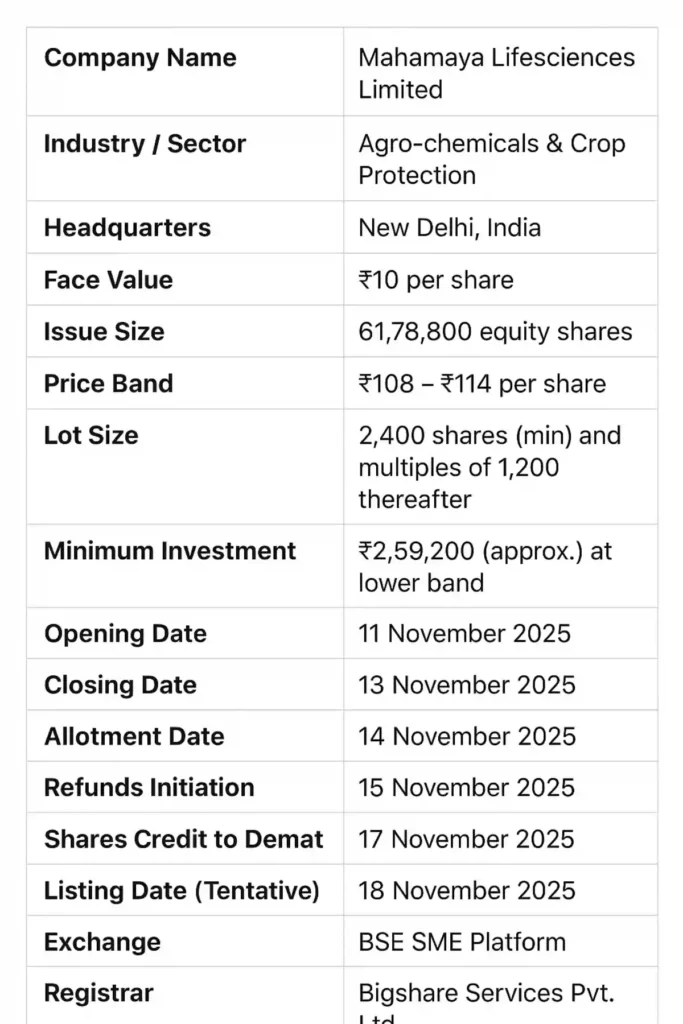

IPO Issue Details

Issue Size and Structure

- Total Issue Size: ₹70.44 crore comprising 61,78,800 equity shares

- Fresh Issue: 56,38,800 equity shares aggregating to ₹64.28 crore

- Offer for Sale (OFS): 5,40,000 equity shares aggregating to ₹6.16 crore

- Krishnamurthy Ganesan (Promoter): 3,70,000 shares

- Lalitha Krishnamurthy (Promoter): 1,70,000 shares

Price Band and Lot Size

- Price Band: ₹108 to ₹114 per equity share

- Face Value: ₹10 per equity share

- Minimum Lot Size: 2,400 shares

- Minimum Investment for Retail: ₹2,73,600 (at upper price band)

Reservation Categories

| Category | Reservation |

|---|---|

| Retail Individual Investors (RII) | 35% (20,59,200 shares) |

| Qualified Institutional Buyers (QIB) | 50% (29,28,000 shares) |

| Non-Institutional Investors (NII) | 15% (8,82,000 shares) |

| Market Maker | 3,09,600 shares |

Key IPO Dates

| Event | Date |

|---|---|

| IPO Opening Date | November 11, 2025 (Tuesday) |

| IPO Closing Date | November 13, 2025 (Thursday) |

| Anchor Investor Bidding | November 10, 2025 (Monday) |

| Basis of Allotment | November 14, 2025 (Friday) |

| Refund Initiation | November 17, 2025 (Monday) |

| Credit to Demat | November 17, 2025 (Monday) |

| Listing Date | November 18, 2025 (Tuesday) |

Issue Registrar and Lead Manager

- Registrar: KFin Technologies Limited

- Contact: 040-67162222

- Email: mahamaya.ipo@kfintech.com

- Website: www.kfintech.com

- Book Running Lead Manager: Oneview Corporate Advisors Private Limited

- SEBI Registration: INM000011930

- Contact Person: Ms. Alka Mishra

- Listing Platform: BSE SME

Objects of the Issue

The company intends to utilize the net proceeds from the fresh issue for the following purposes:

- Purchase of Equipment for Existing Formulation Plant: ₹3.75 crore

- Setting up New Technical Manufacturing Plant: ₹29.40 crore (largest allocation)

- Construction of Warehouse Building and Purchase of Machinery: ₹2.50 crore

- Working Capital Requirements: ₹18.00 crore

- General Corporate Purposes: Remaining proceeds

The strategic focus on setting up a new technical manufacturing plant (₹29.40 crore) indicates the company’s ambition to backward integrate and reduce dependence on imported raw materials, which currently constitute approximately 79% of total purchases.

Company Financials (₹ in Crores)

Financial Performance Highlights

Revenue Growth Trajectory:

- FY 2023: ₹137.08 crore

- FY 2024: ₹161.57 crore (17.87% growth)

- FY 2025: ₹264.15 crore (63.49% growth)

- Q1 FY26: ₹83.01 crore (strong start)

Profitability Analysis:

- PAT Growth: Profit After Tax surged 148% from ₹5.22 crore in FY 2024 to ₹12.94 crore in FY 2025

- EBITDA Margins: Improved from 6.49% (FY 2023) to 9.22% (FY 2025)

- PAT Margins: Enhanced from 2.73% (FY 2023) to 4.84% (FY 2025)

- EPS: More than doubled from ₹3.26 in FY 2024 to ₹7.60 in FY 2025

Return Ratios:

- ROE: Strong at 26.19% in FY 2025, up from 21.16% in FY 2024

- ROCE: Improved to 23.15% in FY 2025 from 16.16% in FY 2024

- Both ratios indicate efficient capital utilization and strong returns on shareholder equity

Balance Sheet Strength:

- Net Worth: Increased from ₹19.44 crore (FY 2023) to ₹49.42 crore (FY 2025)

- Total Assets: Grew from ₹77.88 crore to ₹188.35 crore

- Debt-to-Equity: 1.18 as of FY 2025, showing moderate leverage

Working Capital and Cash Flow Considerations

The company has experienced negative operating cash flows in recent periods:

- Q1 FY26: -₹1.44 crore

- FY 2025: -₹0.52 crore

- FY 2024: -₹22.66 crore

This is primarily due to significant working capital buildup driven by:

- Inventory increase of ₹49.18 crore in FY 2025

- Trade receivables increase of ₹20.15 crore

- Growing scale of operations requiring higher working capital

The company plans to address this through ₹18 crore allocation for working capital from IPO proceeds.

Grey Market Premium (GMP) Analysis

As of November 6, 2025, the Mahamaya Lifesciences IPO GMP stands at ₹0 (Zero), suggesting:

- Expected Listing Price: ₹114 (at par with upper price band)

- Expected Listing Gain: 0.00%

What Does Zero GMP Indicate?

A zero or flat GMP typically reflects:

- Muted Investor Sentiment: Limited unofficial demand before listing

- Valuation Concerns: Market participants may perceive the pricing as fair-to-expensive

- Wait-and-Watch Approach: Investors preferring to assess post-listing performance

- SME Category Caution: Recent regulatory scrutiny on SME IPOs affecting sentiment

Important Note: Grey Market Premium is an unofficial indicator and not a guarantee of listing performance. The actual listing price may differ significantly based on subscription levels, market conditions on listing day, and overall sentiment.

Peer Comparison Analysis

Listed Peers in Agrochemical Sector

| Company | P/E Ratio | ROE (%) | Revenue (₹ Cr) |

|---|---|---|---|

| Nova Agritech Limited | 16.93 | 12.47% | 296.60 |

| Bhagiradha Chemicals & Industries | 247.63 | 2.03% | 449.75 |

| Mahamaya Lifesciences | 16.25 | 26.19% | 264.15 |

Key Observations:

- Mahamaya’s P/E of 16.25 is competitive compared to Nova Agritech (16.93)

- Significantly superior ROE of 26.19% versus peers

- Revenue size comparable to Nova Agritech

- More efficiently managed than Bhagiradha Chemicals

IPO Valuation Metrics

- Post-IPO Market Cap: ₹266.82 crore (at upper price band)

- Price-to-Earnings (P/E): 16.25x (based on FY 2025 EPS of ₹7.60)

- Price-to-Book (P/B): 4.10x (based on NAV of ₹27.82 as of March 2025)

Broker Recommendations

As of the report date, no major institutional brokers have issued formal recommendations on the Mahamaya Lifesciences IPO. This is typical for SME IPOs which generally receive less coverage from large brokerage houses compared to mainboard offerings.

Independent Analysis – Key Considerations

Positive Factors:

- ✅ Strong revenue growth of 63.49% in FY 2025

- ✅ Impressive profit surge of 148% in FY 2025

- ✅ Improving EBITDA margins (6.49% to 9.22%)

- ✅ High ROE of 26.19% and ROCE of 23.15%

- ✅ Established presence since 2002 with promoter experience

- ✅ Strategic backward integration plans with new technical plant

- ✅ Export market expansion showing diversification

- ✅ Competitive P/E valuation compared to peers

Risk Factors:

- ⚠️ Customer Concentration: Top 10 customers account for 71-83% of sales

- ⚠️ No long-term supply agreements with customers or suppliers

- ⚠️ High dependence on imported raw materials (79% of purchases)

- ⚠️ Negative operating cash flows due to working capital requirements

- ⚠️ Regulatory risks in agrochemical industry

- ⚠️ Zero GMP indicating muted market enthusiasm

- ⚠️ SME platform listing with lower liquidity

- ⚠️ Capacity underutilization at manufacturing facility

Who Should Consider Applying?

Conservative Investors: ⚠️ May want to avoid or wait for listing before taking positions due to zero GMP and working capital concerns.

Moderate Risk Takers: 🔄 Can consider applying for listing gains with a small allocation, given the strong fundamentals and growth trajectory.

Aggressive Investors: ✅ Can apply for long-term investment if they believe in the agrochemical sector’s growth story and company’s backward integration strategy.

Risk Rating: Medium to High (Due to SME category, customer concentration, and working capital requirements)

Strengths and Competitive Advantages

- Niche Product Portfolio: Specialization in Emamectin Benzoate and other technical molecules with limited domestic manufacturers

- Regulatory Expertise: Established relationships with CIBRC for product registrations

- Dual Business Model: Both B2B (technical sales) and branded formulations

- Manufacturing Capability: Own plant at Dahej reduces dependence on third parties

- Growing Export Market: Expanding geographical footprint beyond traditional markets

- Financial Performance: Consistent profitability improvement and strong return ratios

- Experienced Promoters: Over two decades in the agrochemical industry

Challenges and Risk Mitigation

Major Challenges

- Customer Concentration Risk:

- Mitigation: Company has reduced concentration from 83.14% (FY 2024) to 71.35% (Q1 FY26) and expanded into new international markets

- Raw Material Import Dependency:

- Mitigation: Setting up technical manufacturing plant (₹29.40 crore from IPO proceeds) for backward integration

- Working Capital Intensity:

- Mitigation: Allocating ₹18 crore from IPO proceeds specifically for working capital

- Regulatory Compliance:

- Challenge: Need for timely product registrations and renewals

- Company Track Record: Successfully registered multiple products with CIBRC; no reported violations

- Seasonal Demand:

- Nature: Agrochemical demand is monsoon-dependent and seasonal

- Diversification: Expanding product portfolio and export markets

Growth Drivers and Future Outlook

Industry Tailwinds

- Market Growth: Indian pesticide industry expected to grow at 8% CAGR during 2023-29

- Food Security Focus: Government emphasis on agricultural productivity

- Export Potential: Growing global demand for Indian agrochemicals

- Import Substitution: Shift towards domestic manufacturing

Company-Specific Growth Catalysts

- Technical Manufacturing Plant: New facility will enable backward integration, reducing raw material costs and improving margins

- Product Pipeline: Registration of new molecules to expand portfolio

- Export Expansion: Recent entry into USA and Hong Kong markets

- Capacity Expansion: Equipment purchase for existing formulation plant

- Working Capital Improvement: IPO proceeds to strengthen operational efficiency

Revenue and Margin Expansion Potential

Based on the company’s trajectory:

- Revenue Target: Potential to reach ₹350-400 crore by FY 2027 (assuming 25-30% CAGR)

- EBITDA Margins: Target of 10-12% with backward integration

- Export Contribution: Aim to increase from current 4.7% to 10-15%

Valuation Assessment

Is the IPO Fairly Priced?

At Upper Price Band of ₹114:

- P/E Ratio: 16.25x (based on FY 2025 EPS of ₹7.60)

- P/B Ratio: 4.10x

- EV/EBITDA: ~11.8x (approximate)

Comparison with Peers:

- Nova Agritech: P/E of 16.93x, ROE of 12.47%

- Mahamaya: P/E of 16.25x, ROE of 26.19%

Verdict: The valuation appears reasonable to slightly premium considering:

- Superior ROE and profitability metrics

- Strong growth momentum (63% revenue growth)

- Backward integration plans

- However, tempered by customer concentration and working capital concerns

Application Strategy

For Retail Investors (Investment up to ₹2 lakhs)

- Minimum Application: 2 lots = 2,400 shares = ₹2,73,600

- Maximum Application: 2 lots = 2,400 shares = ₹2,73,600

- Strategy: Apply for 1 lot with funds ready, considering zero GMP suggests listing might be at par or slightly below issue price

For HNI Investors

- Small HNI (sHNI): 3-7 lots = ₹4,10,400 to ₹9,57,600

- Big HNI (bHNI): Minimum 8 lots = ₹10,94,400

- Strategy: Given zero GMP, HNIs should evaluate risk-reward carefully; may consider subscribing if they have long-term view

For Long-Term Investors

If you believe in:

- India’s agrochemical growth story

- Company’s backward integration strategy

- Management’s ability to execute expansion plans

Then consider buying on listing if stock lists at discount or apply with 3-5 year investment horizon.

Mahamaya Lifesciences presents a mixed investment proposition. On one hand, the company demonstrates impressive financial performance with 148% profit growth, strong return ratios, and strategic expansion plans. The agrochemical sector offers robust long-term growth potential driven by food security needs and export opportunities.

On the other hand, concerns about customer concentration, working capital requirements, and the current zero GMP suggesting muted investor enthusiasm cannot be ignored. The SME platform listing also brings liquidity constraints compared to mainboard offerings.

Rating: 6.5/10

Recommendation:

- For Short-Term/Listing Gains: ⚠️ Avoid or Cautious – Zero GMP indicates limited listing pop potential

- For Long-Term Investment (3-5 years): ✅ Consider Applying – Strong fundamentals and growth trajectory justify investment for patient investors

- Alternatively: Wait and Watch – Monitor listing performance and subscribe post-listing if stock corrects or shows strong subscription

Risk Profile: Medium-High | Investment Horizon: Long-term (3+ years recommended)

Disclaimer: This article is for educational and informational purposes only. It should not be considered as investment advice. Investors must conduct their own research, evaluate risks, and consult with certified financial advisors before making investment decisions. The author and publisher are not responsible for any financial losses incurred based on this information. Past performance does not guarantee future results. Investments in SME IPOs carry higher risks compared to mainboard IPOs.

Stay updated with more IPO analyses, stock market insights, and investment guides on Clear-IPO.com!