Medi-Assist Healthcare Services Limited is among India’s largest health-benefits administrators, bridging the gap between insurance companies, hospitals, corporates, and policyholders. The company operates a technology-based platform that manages health-insurance claims, cashless hospitalization, wellness programs, and digital health services. Headquartered in Bengaluru, Medi-Assist plays a crucial role in India’s expanding health-insurance ecosystem.

Business Overview

Medi-Assist acts as an intermediary between insurers and healthcare providers, ensuring smooth claim settlements and efficient service delivery. It serves three key segments:

- Insurer Partners: Manages claims, hospital empanelment, and network management for insurance companies.

- Corporate Clients: Provides customized wellness programs and employee health benefits administration.

- Retail and Government Schemes: Handles public health-insurance programs and direct retail health plans.

The company’s strength lies in its large hospital network (over 14,000 hospitals across India), its digital-first processes, and proprietary technology that enables automated claim adjudication, fraud detection, and data analytics.

Financial Performance

Medi-Assist has maintained steady revenue growth and strong profitability margins. The company’s FY2025 results showed significant progress, driven by operational efficiency and technology-led cost optimization.

Table 1: Financial Highlights

| Financial Year | Operating Revenue (₹ crore) | Total Income (₹ crore) | EBITDA (₹ crore) | EBITDA Margin (%) | PAT (₹ crore) | PAT Margin (%) |

|---|---|---|---|---|---|---|

| FY2023-24 | 634.7 | 699.0 | 132.2 | 20.8% | 71.2 | 11.0% |

| FY2024-25 | 723.3 | 747.1 | 154.1 | 21.3% | 91.6 | 12.3% |

Key Takeaways:

- Operating revenue grew ~14% year-on-year.

- EBITDA margin improved slightly due to cost control and digital process automation.

- Profit after tax rose ~29% YoY, indicating improved operational efficiency.

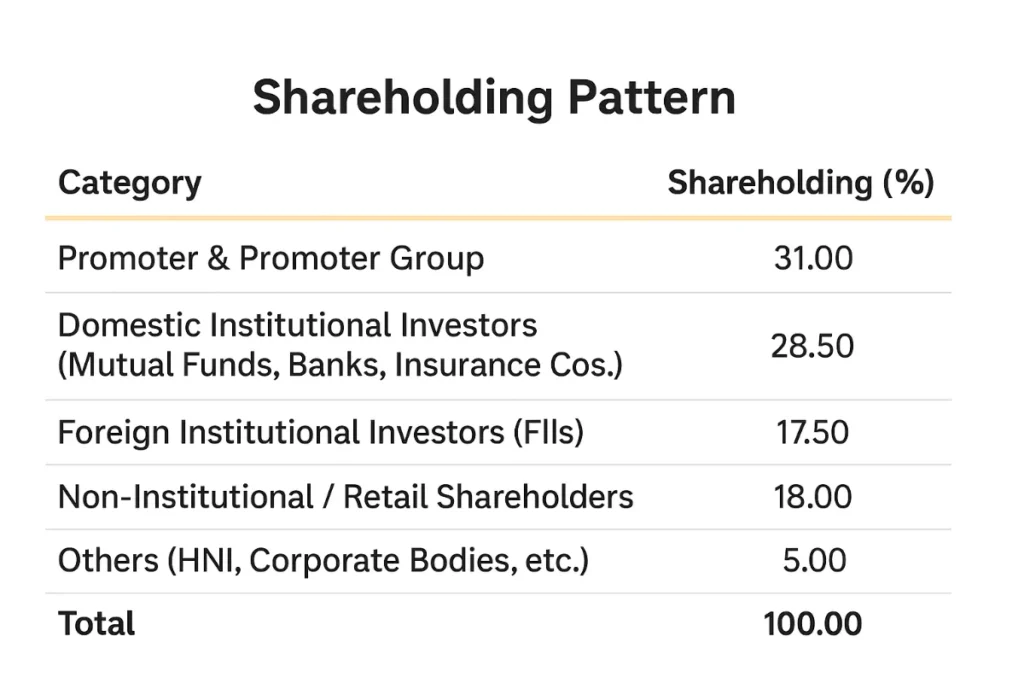

Shareholding Pattern

The ownership of Medi-Assist is well diversified across promoters, institutional investors, mutual funds, and the public. The company also witnessed a significant change in shareholding in 2025 when private-equity investor Bessemer India Capital exited via block deals.

Shareholding Pattern (As of FY2025)

Major Institutional and Fund-House Investors

Several leading fund houses and institutions hold meaningful stakes in Medi-Assist, reflecting confidence in its business model and growth potential.

Major Institutional Holders

| Institution / Fund House | Type | Approximate Holding (%) |

|---|---|---|

| SBI Life Insurance Company Ltd. | Domestic Institution | 4.2% |

| ICICI Prudential Mutual Fund | Mutual Fund | 3.8% |

| HDFC Mutual Fund | Mutual Fund | 3.4% |

| Aditya Birla Sun Life Mutual Fund | Mutual Fund | 2.9% |

| Mirae Asset Mutual Fund | Mutual Fund | 2.3% |

| Foreign Portfolio Investors (combined) | FII | 17.5% |

(Holdings based on latest publicly available filings as of FY2025)

Broker Targets and Recommendations

Medi-Assist has received positive coverage from leading brokerage firms since its listing, with most analysts assigning “Buy” or “Accumulate” ratings. The consensus outlook indicates moderate upside potential driven by consistent revenue growth and digital scalability.

Broker Recommendations

| Broker / Research House | Recommendation | Target Price (₹) |

|---|---|---|

| Nuvama Institutional Equities | Buy | 630 |

| Axis Securities | Buy | 640 |

| ICICI Direct | Accumulate | 615 |

| Motilal Oswal | Neutral | 600 |

| Consensus Average | — | ~630 |

Analyst Sentiment:

The average target price across major brokerages hovers around ₹630 per share, suggesting a stable-to-positive outlook for the next 6–12 months. Most analysts expect steady double-digit revenue growth, supported by margin improvement through automation and new client wins.

Growth Drivers and Outlook

- Rising Health-Insurance Penetration:

India’s health-insurance market is expanding rapidly. As insurers outsource claims processing and digital administration, Medi-Assist stands to benefit from growing transaction volumes. - Technology Advantage:

The company’s proprietary claims platform, real-time hospital validation systems, and AI-driven analytics tools enhance speed and accuracy — key differentiators in the third-party administrator (TPA) space. - Diversified Client Base:

Serving both public and private sector insurers, large corporates, and retail customers reduces business concentration risk. - Profitability & Cost Efficiency:

Medi-Assist operates on an asset-light model with healthy operating margins (around 21%), translating into consistent free cash generation. - Expansion Opportunities:

The company is exploring global tie-ups and tech partnerships to handle cross-border health insurance and wellness services.

Risks and Challenges

- Regulatory Oversight: TPAs are closely monitored by IRDAI, and changes in regulations could affect fee structures.

- Competition: Emerging tech-driven players and insurer-owned TPAs may increase pricing pressure.

- Client Concentration: A few large insurers contribute a significant share of revenue; loss of a key client may impact growth.

Investment View

Medi-Assist has emerged as a steady compounder in India’s digital health-administration segment. With improving operating leverage, rising health-insurance adoption, and strong institutional backing, the company remains fundamentally sound.

The consensus target around ₹630-₹650 offers modest upside potential. Long-term investors looking for stable, technology-enabled healthcare exposure may consider accumulating on dips.